Bank Roll

Setting Your Budget

This should be easy, and you only have to ask yourself one question. What amount of money do you feel comfortable setting aside to have fun betting on sports with and won’t make you uncomfortable if you lose it all? You should pretend upfront that you will never get that money back - forget about it - consider it gone. Look at it as a price you pay to have fun watching sports with a little something extra on the line. Obviously, the point of this site is figuring how not to lose it all and prevent that from happening but hey life happens. There are no guarantees so just make sure you are not risking essential funds that you should be putting towards something else. This is a GAME. There are way more important things in life that you should be taking care of first so please make sure you have the proper perspective here.

We decided upfront when making this site that we were comfortable putting up $5000 as our total sports gambling bank roll. So all of the examples and graphs that you will see below are based off of this as our initial starting budget. If we never see that money again, we will be just fine to go on living our lives without it. But now let’s get into how we plan to do everything we can to make sure that will not end up being the case.

How Much to Bet

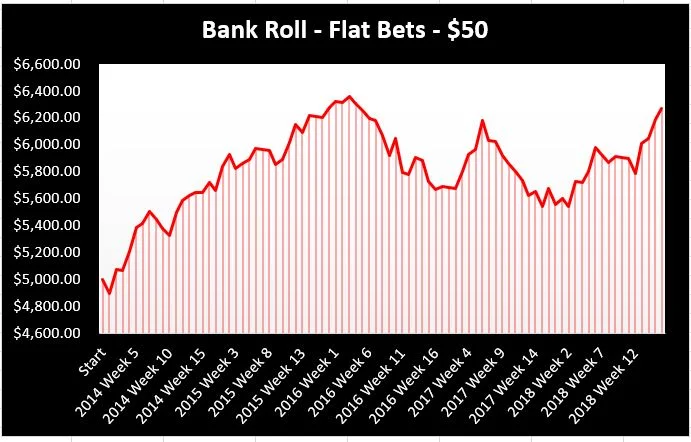

So an initial thought one might have is to just bet a reasonable amount of money on each game without having too much exposure so that you can ride out a cold streak. Sounds simple enough I guess. With a $5000 bank roll, let’s say that we would be willing to bet $50 per game. This would represent 1% of our total bank roll and give us on average about $250 in play per week (see the Betting Strategy page where the back testing shows that we had advantage bets on about 5 games per week over the past 5 years - that’s where the $250 in play per week comes from). Well let’s take a look how that would have worked out over the past 5 seasons.

Not bad. We would have had some ups and downs (more ups than downs) and ended up sitting on a larger bank roll than what we started with - $6309 - which is great. This works out to an average yearly return on investment of 4.8%. At that rate, there are better ways to invest your money for sure, but I doubt it would be as much fun.

Now before we take a look at some other betting scenarios, I just want to make note of a few things with regards to the bank roll graph.

Three out of the five seasons resulted in solid positive growth (2014, 2015, 2018)

One of the seasons was fairly neutral ending up with only a slight loss (2017)

The 2016 season was rough! We basically wiped out all of our winnings from the season before (ouch!).

Our peak bank roll ($6364) actually occurred at the beginning of the 2016 season. It took us a couple of seasons to climb out of the hole that 2016 left us in.

The below table shows the season by season record on our advantage bets (bets where our model predicted the line 4 or more points off of the closing line). For a detailed look at our bet history, see the historical NFL seasons sections where we list out the bets that would have been made for the past 5 years utilizing our model and the ensuing results.

This really highlights just how bad that 2016 season was, but it’s a great lesson that reminds us there will be some periods of bad luck. That’s the nature of playing a game where you are only right about 55.56% of the time. While the 2016 season is certainly a bit of an outlier, it is still well within the realm of possibility. Assuming a win rate of of 55.56%, we could expect to have a betting season like that about 1 in every 28 years. So be prepared. Our overall trend should be heading in the right direction but we may have to take some lumps along the way. I’m actually glad to see it happen this way in the little back testing that we completed because it should give us confidence to weather the storms in the future rather than giving up at the first sign of trouble.

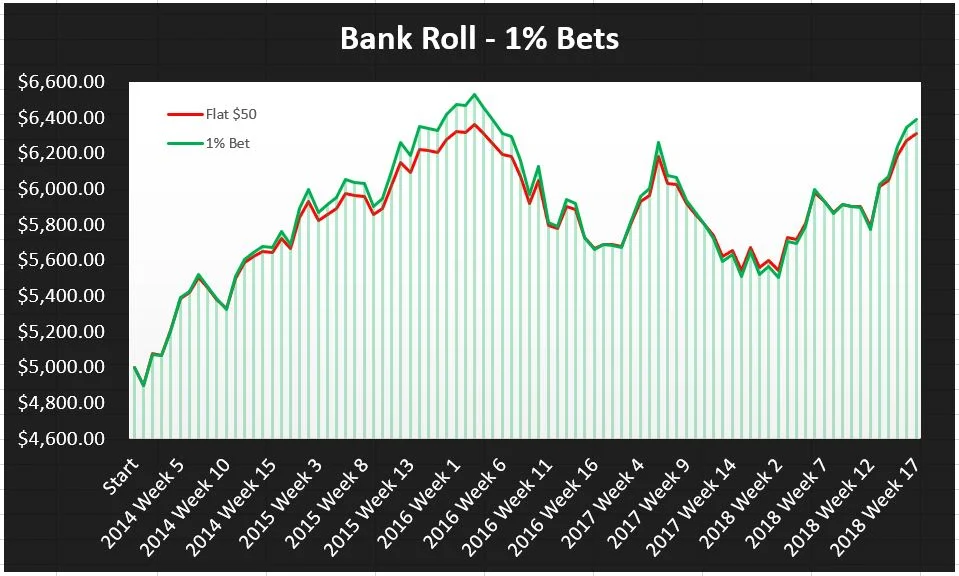

All right so we have looked at what a static $50 bet across all the advantage games for the last 5 seasons would have gotten us. Not a bad result, but we can definitely do better. The first thing that comes to mind is why don’t we at least adjust our bet size based on our bank roll. If we feel good about betting $50 with a $5000 bank roll, we should feel just as good betting $60 with a $6000 bank roll (maintaining a 1% bet). Here’s what that would look like below (bet size adjustments made weekly based on bank roll size prior to that week’s games).

All right - moving on up…slightly. Things are getting a bit better for us. Our ending bank roll is now $6390 which equates to an average ROI of 5.0% per year. A respectable return but certainly nothing to get too excited about. One thing to notice about the graph is that betting a percentage of your bank roll starts to amplify the peaks when things are going well. It also shows that our valleys are just slightly lower. This is because we are making bigger bets than the flat $50 bet ever since we started climbing above of our initial $5000 bank roll. In theory, if we were to ever to hit a real bad streak and drop below our initial bank roll of $5000, the valleys would not be as deep by betting 1% of the bank roll. The bet size would then be below the flat $50 line and save us from losing as quickly which is the main advantage of basing your best on a bank roll percentage. This will help us out and save us some money if we end up having a bad start to the 2019 season.

The truth is, both of these scenarios are a bit on the conservative side if we really think we have an edge. It’s time to look at something a bit more aggressive. Enter the Kelly Criterion. For a brief overview, check out the Terminology page of the site. Right here, we are just going to jump right into it. The following formula is a way to determine the optimum bet size to maximize your bank roll when you have an accurate prediction of what your win rate will be.

So we know what our expected win rate should be based on the last 5 seasons of back testing and that is 55.56%. Plugging this into the formula as shown above yields an optimal bet size of 6.7% of our bankroll. Using this as our guide, the following graph shows what our bank roll would look like if we had bet following the Kelly Criterion.

Wow! Now that is a roller coaster ride! The ending amount is definitely still a real nice improvement over our 1% betting strategy. We now have a final bank roll of $13853 and an excellent return on investment of 22.6%. Nearly any investment manager would love to lock in that kind of return over 5 years if it was offered to them.

But damn we would need to have some serious stones to weather that 2016 and 2017 season betting like this. Our bank roll would have actually peaked at about $23000 near the beginning of the 2016 season. After that though, it is a brutal drop to around $6000 at the end of the 2017 season. We never dipped below our initial starting bank roll, but that would have been a real rough ride.

So that’s still a pretty nice performance if we stay committed to the full Kelly Criterion approach shown above. Even though we are pretty satisfied with this, something kept popping out at us when looking at the following chart of our back testing results:

So our overall win percentage for games with a spread differential off of our model by 4 or more points is 55.56%. It would make sense that the further off the model prediction is from the actual spread, the better it should do. The chart above demonstrates this pretty clearly. The success with games that are greater than 8 points off of our model is significantly better than the games in the 4 to 8 range, and those games in the 4 to 8 range are better than the ones below 4. This leads us to believe that maybe the best approach is to separate our picks into these three main categories, give them dumb names like Sharp Bet and Razor Sharp Bet, and utilize the Kelly Criterion betting approach to bet accordingly on each grouping. The table below summarizes this thought.

All right so let’s what our bank roll would have look liked with the betting strategy from the table above. We will call it the Tiered Kelly Criterion approach.

Whooaaa!!!!!

It almost doesn’t seem real. That’s a final bank roll of $57666 with an ungodly average ROI of 60.3%. Enough to make any Wall Street money manager insanely jealous. We are gonna make a killing!

Hmm… maybe we should pump the brakes just a little bit here.

We did luck out a bit that the 2018 season happened to end on such a nice peak. We were definitely hot at the end of the year. So what if we looked at where our bank roll was at in one of the troughs instead. After Week 2 of the 2018 season, we hit a low point of $13343. That’s still good for an extremely respectable 21.7% ROI. So all in all, it looks like we are still in pretty good shape with this model. Before we start popping bottles, there is one more thing we should consider about utilizing the Kelly Criterion that we’ll talk about below.

The important qualification of making sure the Kelly Criterion formula works is that you must have an accurate prediction of what your win rate will be. Well, we know what our win rate WAS for the past 5 seasons, but can it continue? Based on the fact we have 444 data points so far, we can feel decent about the same win rate continuing in the future, but it could easily be a bit less or a bit more. That’s well within the realm of possibility. Most people like to have at least 1000 data points before making too many predictions so that is why we do plan to continue our back testing further into the past but for now we are heading into the 2019 season with what we have so far. With that in mind, do we really want to be straddling that line (the Kelly Criterion establishes that line) between massive success and possible bankruptcy of our bank roll? We love to gamble, but we also know when to show a little restraint. Let’s just imagine that we were a little bit off on our predicted win rate - say a half standard deviation or even a full standard deviation lower than what we are showing through the 5 seasons of back testing. Below is a graph showing the results if we would have bet the suggested Kelly Criterion amounts above but had performance a half a standard deviation or a full standard deviation below the back tested win rate:

Yikes! Looks like we would have only barely survived that 2016-2017 run of bad luck if we were a full standard deviation off. That’s the danger of the Kelly Criterion. You have to be spot on with your predictive win rate for it to work out to that optimum scenario we showed above. If you are a bit too aggressive, your bank roll could spiral down fast.

All is not lost though. Just because we may not want to bet the full amount that the Kelly Criterion suggests on all of our games, we can take a safer approach and just bet a portion of what is suggested. This will give us some safety factor and tolerance around our predictive win rate. Let’s see what would happen if we bet half of what the Kelly Criterion suggests (from now on we will just refer to this as the Half Kelly approach while following the Kelly Criterion suggestion to a ‘T’ will be a Full Kelly). Below is the graph of a Half Kelly approach with the win rate back to where we would expect it to be.

Ok ok - we may not have to change our pants immediately after looking at this graph, but it still produces a very respectable result. A final bank roll of $25294 and a yearly ROI of 38.3% is nothing to scoff at. So let’s see how this Half Kelly approach protects our bank roll in the lower win rate scenarios we ran above that were 1/2 to 1 full standard deviation lower than expected. This is where the Half Kelly approach should shine and show its value versus going aggressive with the Full Kelly strategy.

After looking at the graphs and the comparison table above, we are leaning towards this Half Kelly approach as a good compromise to protect ourselves a bit during the down times. If we take this approach and our win rate is worse than we thought, we can still make decent money and avoid the risk of losing long term. The $10024 vs. $5745 3rd column is what catches our attention the most. Even if we are 1 standard deviation off on the expected win rate, we can still double our money over 5 years (roughly 15% ROI). Now this is probably the point where we should do some Monte Carlo simulation to determine what the optimum Kelly % would be with an acceptable level of risk to maximize our potential outcomes. But that’s something we still need to learn a bit more about so we are planning it for a feature article at some point during the season. Depending on the results, we may end up changing our approach somewhat from a Half Kelly betting strategy to something a bit more aggressive or conservative. For now, the Half Kelly it is. The Half Kelly bet percentage is equivalent to the Full Kelly recommendation at a win rate of 53.2% for Sharp Bets and 58.1% for Razor Sharp Bets. As long as our future performance stays above that, we will be winning money and showing positive growth of our bank roll.

Well, there you have it. It looks like we found our betting strategy for the upcoming seasons. It took us awhile to get there, but we are feeling pretty good heading into 2019. Our starting bank roll is set and we are ready to capture some of these returns!